Global Launches: Trends, Observations, and Opportunities

This is a launch activity analysis. If you’re looking for a spacecraft deployment analysis (and possible opportunities), please go to the “Spacecraft Trends and Increasing Opportunities” article.

Things are changing in the global launch landscape. Specifically: more launches than ever are happening. Smallsat launches and rideshares are increasing. More mass is going into the Earth’s orbit. Reusability is a thing (at least for two companies).

And yet, things haven’t really changed.

Despite assertions of increased competition in the marketplace, launch providers are essentially operating from the same nations now as they did five, ten, and 15 years ago. That also means that the active orbital launch spaceports are very much the same (Wenchang in China and Mahia in New Zealand are the exceptions).

And in 2023, with few exceptions, the same companies and agencies are launching some of the same rockets that were developed longer than 15 years ago. A few of the legacy companies’ attempts to field new rockets have been… problematic.

In the global launch industry, some things have changed then, while others remain the same.

Launch Activities: Ups and Downs Towards Up

As of 31 July 2023, launch service providers from eight nations successfully launched 109 rockets that have deployed nearly 2,000 spacecraft into the Earth’s orbit for 2023. Eighty-eight rockets were launched during the same period a year earlier, in 2022. The 109 launches are an ~24% increase from rockets launched the year prior.

The seven months of successful launches in 2023 have already exceeded the total successful orbital launches for the years 2019 (98 launches) and 2020 (104 launches). Both years were below 2018’s 112 successful launches, but the general trend from January 2019 through July 2023 is upward.

Since the number of launches from January through July 2023 has already exceeded launches from the same period in 2022, then 2023 will likely continue the wavy upward climb past 2022’s total launches. At least it should--barring any disaster, accident, or global health crisis.

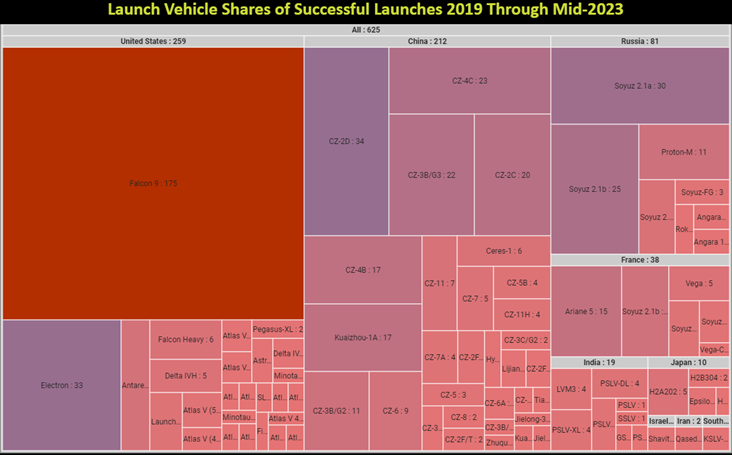

SpaceX’s Falcon 9 contributed significantly to that growth. Glancing at the treemap below shows how much SpaceX’s rocket is a part of global space activities.

The treemap above depicts all successful launches conducted from January 2019 through July 31, 2023. Launch service providers conducted 625 launches during that time, with SpaceX’s Falcon 9 taking 28% (175 launches) of all launch activities.

Adding the Falcon Heavy to the mix (6 launches) gives SpaceX an ~29% share of the world’s launches during that time. It’s incredible that six additional launches barely add a percentage point to SpaceX’s overall launches.

Launch Observations: Reusability and Air-Launch

Taking out the 97 Starlink launches from that total still results in the Falcon 9 with a dominant share of ~15% (78 launches) of the world’s successful launches—not too shabby for a relative newcomer. In 2023 alone, Falcon 9 accounted for 9% (48 launches) of the world’s launch activities in the past 4.5 years.

Based on the treemap, what we see with the Falcon 9 and Falcon Heavy is that there is only one reusable orbital launch system out of 80+ rockets used globally. Rocket Lab is still stepping toward reusability with its Electron, but no one else has a reusable operational orbital rocket.

The high frequency and the number of Falcon 9 launches also point to a few of the strengths of a reusable system: accessibility and flexible scheduling. Both answer customer challenges that other launch providers won’t provide.

A launch service provider with a reusable rocket system doesn’t need to build a rocket for every launch. In Falcon 9’s case, SpaceX is building upper stages for each launch, but not the first stage. That protects the company from several operations bottlenecks—manufacturing, transportation to the launch site, etc.

A reusable system also allows a company to, with practice and experience, quickly turn around used boosters for other launches. With first-stage boosters appearing to be available at nearly any given time, the company can use the weakness of its competitors—slow operations and schedule holes. It can schedule launches in those gaps (which SpaceX appears to be doing).

This SpaceX capability raises the question—why aren’t more competitors pursuing reusability? Not just engine reusability, as suggested for Vulcan, but, at the very least, first-stage reusability.

The initial reason floated by legacy providers was that it wasn’t clear reusability was good for their business. But they were referencing the development and recovery costs. It seems clear that reusability offers more good reasons than that.

The customer options that reusability brings might lead the cynical to believe that the other launch providers who aren’t pursuing that capability are not interested in growing their customer base. They don’t appear intent on keeping current ones, given the U.S. Department of Defense’s desire to launch no-notice at basically any given time.

Another data point is that nearly all launch providers launch their orbital rockets vertically. Only two U.S. launch operators, Northrop Grumman and Virgin Orbit, deviated from that, launching rockets from aircraft instead.

Virgin Orbit went bankrupt early in 2023, taking LauncherOne out of operation. Northrop Grumman lists its Pegasus on its website but has only two in inventory. None of the remaining world’s operational launch service providers offer aircraft-launched orbital rockets, and none appear to have plans for such a rocket.

Other launch service providers may not have embraced air-launched rockets for a simple reason: added complexity with little return. Both Pegasus and LauncherOne had low upmass capability. They required pilots and crew for aircraft in addition to launch crews. The support infrastructure for maintaining and flying aircraft costs money. Those complexities might make sense when using a fleet of aircraft but not when using one, such as Virgin Orbit’s single 747.

Both companies advertised the ability to launch from any runway that supports their aircraft. Still, that capability didn’t seem to interest prospective customers (except perhaps those running government military and civilian missions).

These factors add up to why startups aren’t pursuing air-launched rockets. Pure rocket science, it turns out, is more straightforward than rocket science with aircraft thrown in.

Smallsat Launch Activities: Middling Usage

For this analysis, smallsat launchers have a maximum upmass capability of 1,500 kilograms. Smallsat launches throughout the past 4.5 years are a little more complicated. Looking at the trend during that time, there is some growth in using smallsat launch systems. However, the change is modest compared to overall launch growth during the same period.

The total launches on the Y-axis for orbital smallsat rockets are significantly smaller than the Y-axis in the chart describing overall successful orbital launches. The time series chart above does not include rideshares from larger launch vehicles such as China’s CZ-2D or the U.S. Falcon 9.

The chart shows that the monthly average for two and three-quarter years (29 months) for smallsat launches was more than one. It may be that the rise in monthly launches started after May 2021, when no launches occurred.

Several newcomers have stepped into the smallsat launch service arena, including the company taking the largest share of launches since January 2019: Rocket Lab.

Of 625 successful orbital launches between 1 January 2019 and 31 July 2023, smallsat launches (101 launches) accounted for a ~16% share. The treemap above shows that smallsat launch service providers from two nations--the United States and China--dominated smallsat launches, taking ~88% (89 launches) during that period.

China’s smallsat launches (48 launches) edged out the U.S.’ (41 launches). So many smallsat launchers in China may indicate that other regions are underserved (or China’s launch providers are overserving it).

Smallsat Launch Observations: Mass, Reusability, and Rideshare

However, while smallsat launchers like Arianespace’s Vega or IHI’s Epsilon were launched less, they also have about five times the upmass capability of the two most launched smallsat rockets.

For example, Rocket Lab’s 32 Electron launches deployed over 140 spacecraft, but Vega deployed slightly over half that (75 spacecraft). It deployed them using only five launches, ~16% of Electron’s launches to deploy 140 spacecraft.

The tug-of-war for customers between launchers like Electron and Firefly’s Alpha is likely to continue if the larger launchers become reliable and start launching more often.

Electron launched nearly double the launches of its closest competitor in the past 4.5 years, the Kuaizhou-1A from CASIC’s ExPace Technology Corporation. Both rockets have the same upmass limitation of 300 kilograms. The technology Kuaizhou-1A uses to get satellites to orbit differs, relying on solid rocket motors. The Electron uses liquid propellant instead.

Only one active smallsat launch service provider is pursuing some kind of reusability: Rocket Lab. Rocket Lab is experimenting with its Electron for reusability, recovering the spent booster from the ocean and refurbishing it for reuse. The experimentation provides Rocket Lab with some reusability experience when the company begins testing its planned reusable Neutron rocket.

The seeming lack of interest in reusability from other smallsat launch manufacturers might be due to mass concerns. A smallsat launcher, especially a rocket that can lift only 200-300kg, doesn’t have much overhead for additional equipment to provide reusability. If a company can design a rocket with useful upmass and reuse capability, that might revive interest and rivalry toward implementing reusability.

Based on SpaceX and its competitors’ reactions—perhaps not.

An unexpected data point is the impact of larger rockets that offer ridesharing to smallsats. Rockets such as India’s Polar Satellite Launch Vehicle and Soyuz 2.X offered ridesharing opportunities to consumers early on, but the smallsat launch average stayed pretty even through September 2021.

In January 2021, SpaceX began launching dedicated smallsat rideshare missions for very little money. One might have expected SpaceX’s program to steal customers from the dedicated smallsat launch providers.

Instead of cannibalizing the smallsat customers and impacting smallsat launches, both launches and customers increased from zero smallsat launches in May 2021. As noted before, that growth is modest, averaging slightly more than two smallsat-dedicated launches per month. While almost a doubling of the average from the previous 29 months, it’s still not much more than two per month.

Again, it’s not a decrease in dedicated smallsat launches one might have expected due to the entry of SpaceX and its Smallsat Rideshare Program. Instead, the average increased.

Part of that increase might be explained because most of the dedicated smallsat launchers were launched from China. The launch companies and organizations in China don’t compete for smallsat operators (aside from within China). Very few smallsat operators from outside nations use China’s launch offerings.

Spaceports

There are few new and active orbital spaceports in the world. Twenty-one conducted launches sometime during the past 4.5 years. Red bubbles on the map represent launch activity from each spaceport. The larger the bubble, the more active the spaceport (and launch pad).

For 2023 so far, less than half (10) of the available active orbital spaceports have hosted launch activities. Generally, the launch activities from those spaceports appear the same.

The most active orbital launch area in both maps is in Florida, where the state hosts launch activities from Cape Canaveral Space Force Station and Kennedy Space Center. While they are two different spaceports with some distinctions, they function similarly, face similar challenges and climate, and host (mostly) the same launch operators.

While China’s launch bubbles are smaller, the nation’s four spaceports aided its launch operators in maintaining the second-highest number of launches for the past 4.5 years, including 2023.

Rocket Lab’s New Zealand’s Mahia Peninsula site and China’s Wenchang Space Launch Site on Hainan Island are the newest orbital spaceports.

The overall lack of new orbital launch spaceports may be because current spaceports are underused. Russia and the U.S. have launch pads available in their spaceports and infrastructure to support new and existing space launch providers.

Advocates of new spaceports fail to mention this competitive aspect of their competitors, seeming not to consider the billions of dollars in upgrades to those legacy facilities and the experienced support they bring.

Despite launch growth (unless a nation funds its own space program), existing spaceports are the most accessible and logical option for most launch providers. Until they get too busy with launches (which isn’t the case currently).

John Holst is the Editor/Analyst of Ill-Defined Space, dedicated to analysis of activities, policies, and businesses in the space sector.

Contact Astralytical for your space industry analysis and insight needs.